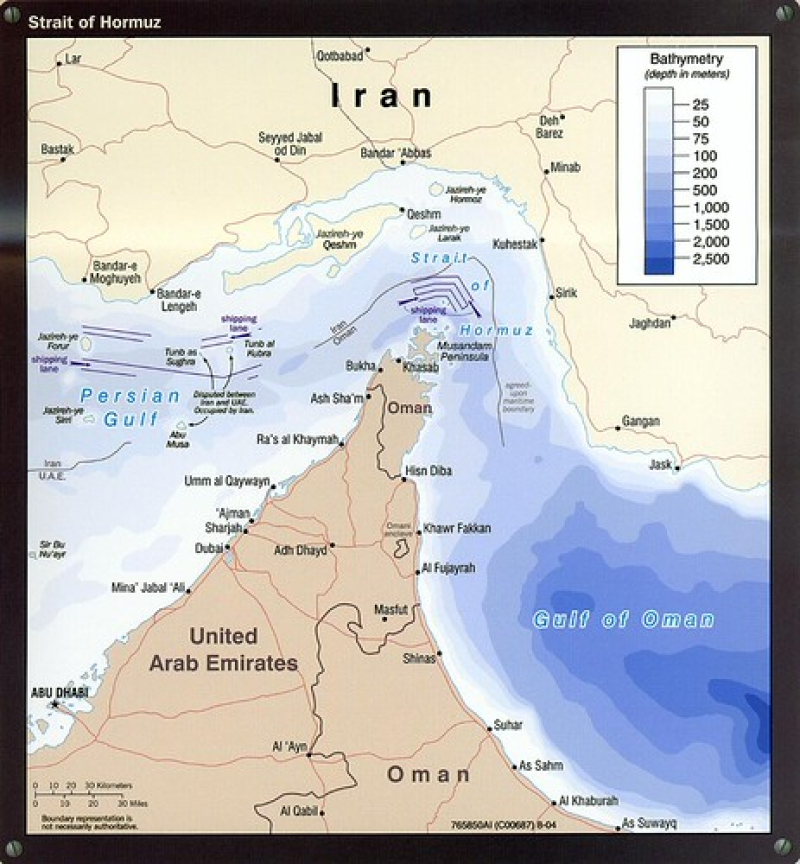

The Strait of Hormuz no longer has one authority. For commercial shipping, that contradiction is now the operating environment.

The dispute is not simply rhetorical. Washington has sanctioned the PGSA, conducted covert escort operations for more than 200 commercial vessels, and Treasury Secretary Bessent has pledged to claw back any transit fees paid to Iran from frozen Iranian assets.

Tehran, meanwhile, is reportedly making Hormuz sovereignty recognition a condition of broader peace talks. The strait has become a negotiating chip with a naval garrison on each side.

The first and most straightforward is alignment with the US corridor. CENTCOM has established designated transit pathways with military escort, and the Bessent offset mechanism means PGSA tolls are financially worthless if the US can recover equivalent sums from Iranian accounts.

This is the posture Washington is actively rewarding and the one most Western majors are adopting. The risk is that it is entirely dependent on sustained US military presence. If Washington’s force posture shifts, the corridor collapses.

The second option is PGSA permit compliance. This is already the de facto posture of the shadow fleet and Chinese-aligned tonnage. Operators obtain Iranian transit authorization, hand over operational data to IRGC-coordinated authorities, and move their cargoes without US military contact.

It carries severe Western sanctions exposure, no Western insurance coverage, and the Bessent mechanism makes the permits financially self-defeating. But for operators whose buyers and flag states sit outside the US-led order, it remains a functional option.

The third is going around. Cape of Good Hope rerouting adds ten to fourteen sailing days and significant bunker costs, but it exits the jurisdiction contest entirely. For cargo that does not originate or terminate in the Persian Gulf, this is increasingly rational.

It will structurally disadvantage Eastern Mediterranean transshipment hubs and redraw the economics of Indian Ocean logistics consequences that extend well beyond Hormuz.

A fourth posture dual-authorization hedging is being attempted by some larger operators: maintaining PGSA permits as an option while publicly complying with the US corridor.

This is legally treacherous and operationally fragile. As Treasury enforcement tightens, the ambiguity space contracts. Operators in this posture face a forced binary choice within roughly 60 to 90 days.

The fifth scenario a negotiated settlement that produces a recognized, internationally monitored transit framework is structurally transformative but currently improbable. Iran wants sovereignty recognition; the US has built a unilateral architecture it considers sufficient and is financially undermining Iran’s toll system.

The probability rises only if indirect talks formally table Hormuz as an agenda item, or if a major incident generates irresistible pressure for neutral mediation.

What makes this moment structurally different from previous Hormuz crises is that the bifurcation is hardening by the day.

Each vessel that transits under US escort, each tanker disabled by CENTCOM in the Gulf of Oman, each PGSA permit issued to a Chinese-bound crude cargo deepens the operational reality of two incompatible systems. Shipping’s geography is fracturing along the same lines as the broader geopolitical competition.

What we have is a new structural condition of maritime commerce and the industry is only beginning to price it in.