Two developments surfaced within 24 hours of each other last week, and read together they describe the exact phase the Hormuz corridor has now entered: fast, real recovery on the water, and a stubborn reminder that recovery is not the same as safety.

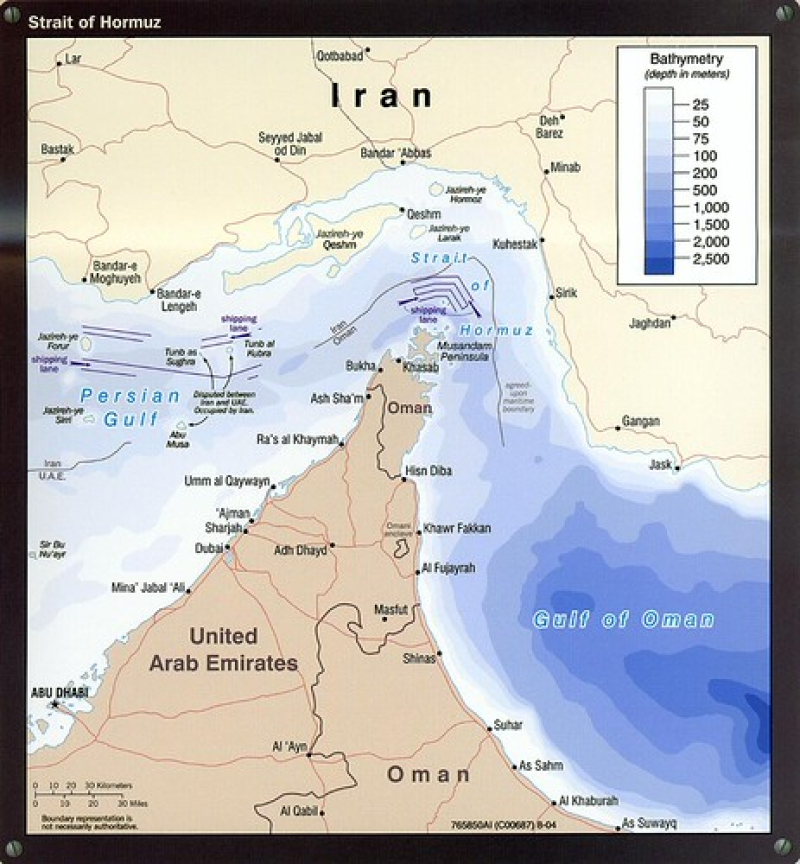

At least five supertankers carrying ten million barrels of Saudi crude cleared the Strait of Hormuz after loading resumed at Ras Tanura, the world’s largest oil port, following a nearly four-month shutdown tied to the Iran conflict.

Aramco has switched to spot pricing to move the barrels quickly, offering six million barrels to Asian buyers on terms traders describe as unusually attractive.

Roughly 76 nautical miles south of Balhaf, Yemen, just outside the Strait in the Gulf of Aden, a merchant vessel was boarded by four armed individuals carrying a rocket-propelled grenade.

They damaged the bridge before departing; the crew reached the citadel safely. Two hours later and nearby, a second vessel reported a small craft shadowing it before turning away. The incidents came one day after regional monitors had logged zero confirmed incidents across the prior 48 hours.

Set against this series’ scenario work, neither development is a surprise. The dominant post-ceasefire pathways were always a phased diplomatic return or a managed corridor without full settlement, not a full multilateral resolution, which was treated from the outset as the least likely outcome.

Ras Tanura’s ramp-up is the managed-corridor scenario: physical throughput and price competition recovering well ahead of any durable authorization architecture.

The Balhaf boarding fits an equally established pattern. Earlier analysis in this series concluded that certain armed threats survive conventional de-escalation and tend to activate precisely when carriers are most inclined to relax, a dynamic borne out when prior Hormuz seizures also landed just after a ceasefire took hold. That pattern is repeating now, one waterway over.

What last week’s news actually shows is a decoupling: Hormuz-proper normalizing operationally while its Gulf of Aden approaches keep carrying an unresolved, low-level security risk that ceasefires do not touch.

War-risk insurers are likely to price the two zones differently as a result, premiums easing on the Hormuz-proper route even as a separate loading holds for the Aden approach.

There is a wider signal in this too. Chokepoint states beyond the Persian Gulf are watching whether large-scale commercial flow can resume even while armed disruption capability persists nearby, unaddressed.

If it can, if the industry absorbs incidents like Balhaf as a cost of doing business rather than a reason to pause, that is itself a template, and one with relevance well past Hormuz.

The more durable finding is that recovery, in this corridor, has never meant the underlying risk disappeared, only that the industry has learned to sail past it.